Is 2 Percent Cash Back a Lot in Commercial Property Sales?

Feb, 27 2026

Commercial Property Cash Back Calculator

Calculate Your Cash Back Value

See exactly what 2% cash back means for your specific deal size. Input your property value to see real dollar amounts and contextual value.

Enter your deal size to see results

Is This Enough?

1-2% is common

Can cover closing costs

1.5-2.5% is standard

Typically $75k-$500k

0.5-1.5% is typical

Often $100k-$300k

When you're buying or selling commercial property, every dollar counts. So when someone mentions 2 percent cash back in a deal, you might wonder-is that actually worth it? Or is it just a flashy perk that doesn’t move the needle? The answer isn’t simple. It depends on the size of the deal, who’s offering it, and what you’re really trying to achieve.

What Does 2 Percent Cash Back Even Mean?

Cash back in commercial real estate usually comes from the broker, lender, or sometimes the seller. It’s not a rebate from the government or a tax credit. It’s money handed back to you after the transaction closes-often as a lump sum. For example, if you buy a $5 million office building and get 2 percent cash back, that’s $100,000 in your pocket after closing.

That sounds like a lot. And on paper, it is. But here’s the catch: cash back isn’t free money. It’s often baked into the deal. Maybe the seller raised the price by $100,000 so they could give it back to you as an incentive. Or maybe the broker is reducing their commission to sweeten the deal. You’re not getting extra cash-you’re just getting some of your own money back.

Is 2 Percent Good Compared to Industry Standards?

In commercial real estate, standard commissions for brokers range from 4 to 6 percent of the sale price. That’s paid by the seller. But when a buyer’s agent offers cash back, it’s usually a portion of their commission-often 1 to 3 percent. So 2 percent falls right in the middle of what’s typical.

Here’s how it breaks down in real deals:

- Small deals ($1M-$5M): 1 to 2 percent cash back is common

- Mid-size deals ($5M-$20M): 1.5 to 2.5 percent is standard

- Large deals ($20M+): Cash back drops to 0.5 to 1.5 percent because the dollar amount is already huge

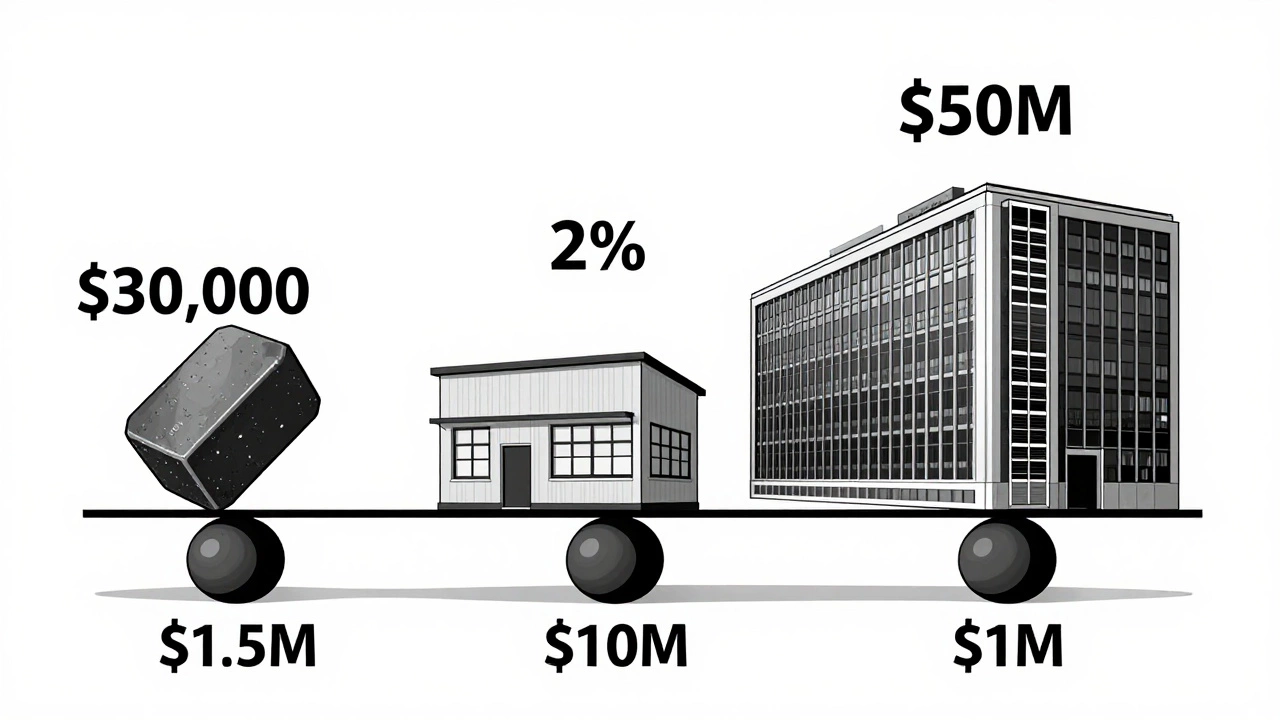

So if you’re looking at a $10 million warehouse and someone offers 2 percent ($200,000), that’s not unusually high-it’s actually average. But if you’re buying a $1.5 million retail space and get 2 percent ($30,000), that’s a solid incentive. In smaller deals, even 1 percent can cover closing costs, inspections, or legal fees.

Who’s Really Offering the Cash Back?

Not all cash back is created equal. The source matters a lot.

Broker cash back: This is the most common. A buyer’s agent gives you a portion of their commission. It’s legal and common, but make sure it’s disclosed in writing. Some agents use it to win your business, especially in competitive markets like Los Angeles or Chicago.

Seller cash back: Rare, but it happens. A seller might offer it to close a deal faster or if they’re desperate. But this often means the price was inflated. Always ask: “Is the purchase price higher because of this?”

Lender cash back: Some commercial lenders offer cash back as a closing incentive. This usually comes with higher interest rates or fees. Watch out-it’s not a gift. It’s a trade-off.

Always get the offer in writing. If a broker says, “I’ll give you 2 percent back,” but doesn’t put it in the contract, it doesn’t exist.

What Can You Actually Do With 0,000 (or 0,000)?

Let’s say you bought a $5 million industrial property and got 2 percent back-$100,000. That’s not pocket change. Here’s what that money can realistically do:

- Pay for $80,000 in tenant improvements (new flooring, lighting, HVAC upgrades)

- Cover $15,000 in legal and title fees you didn’t budget for

- Set aside $5,000 for emergency repairs in the first year

That’s not just a bonus. That’s money that improves your cash flow, reduces your out-of-pocket costs, and makes the property more valuable from day one.

Compare that to a deal with no cash back. You’d have to pull that $100,000 from your own reserves. That means less liquidity, slower reinvestment, or even delayed renovations. In commercial real estate, timing matters. Getting cash back upfront can be the difference between upgrading a building in Month 2 versus Month 14.

When 2 Percent Isn’t Enough

There are times when 2 percent feels like a slap in the face.

If you’re buying a $50 million data center, 2 percent is $1 million. Sounds great, right? But if the seller is also asking for a 10-year lease with no rent escalations, or if the property needs $3 million in roof and electrical upgrades, then $1 million doesn’t go far. In those cases, you’re better off negotiating lower price, better financing, or seller-funded improvements.

Also, if the cash back comes with strings attached-like requiring you to use a specific lender or property manager-it’s not really a benefit. It’s a trap.

Always ask: “What am I giving up to get this?” If the answer is a higher purchase price, longer lease terms, or hidden fees, walk away.

How to Negotiate Better Than 2 Percent

If you’re serious about maximizing value, don’t settle for 2 percent just because it’s common. Here’s how to push for more:

- Compare multiple brokers. If three agents are bidding for your business, the one offering 2.5 percent might be the one who actually works harder.

- Use market data. Show them recent comparable deals where buyers got 2.5 percent. In LA’s industrial market, that’s not unusual.

- Bundle it. Ask for 1.5 percent cash back + seller-paid closing costs. Sometimes they’ll say yes to the combo even if they won’t raise the cash back alone.

- Time it right. In a buyer’s market (like early 2026, with interest rates still high), sellers and brokers are more willing to sweeten deals.

Don’t be afraid to say: “I’ve seen 2.5 percent on similar properties. Can you match that?” Most brokers will try.

Red Flags to Watch For

Not all cash back offers are honest. Here’s what to watch out for:

- The purchase price went up right after the cash back was mentioned

- The broker won’t show you the commission breakdown

- You’re pressured to sign quickly-“This offer expires tomorrow”

- The cash back is paid in credits, not actual cash

If any of these happen, get a second opinion from a commercial real estate attorney. A good one can review the contract in under 24 hours.

The Bottom Line

Is 2 percent cash back a lot? In most commercial property deals, it’s solid-but not exceptional. It’s the baseline. If you’re buying something under $5 million, it can be a game-changer. If you’re buying something over $20 million, it’s a nice bonus but won’t change your strategy.

The real question isn’t whether 2 percent is a lot. It’s: What did you give up to get it? If the price is fair, the terms are clean, and the money lands in your bank account without strings, then yes-it’s a win. If not, you’re just rearranging deck chairs on a sinking ship.

Always run the numbers. Calculate what 2 percent means in real dollars. Then ask: “Would I still make this deal if the cash back disappeared tomorrow?” If the answer is yes, you’ve got a good deal. If the answer is no, you were seduced by a perk-not a strategy.