What Does NOI Mean in Commercial Real Estate? A Simple Guide

Jun, 20 2026

Commercial Real Estate NOI Calculator

Calculate Net Operating Income (NOI) and estimated property value based on Cap Rate.

You’ve seen the number on every listing. It’s bold, it’s prominent, and if you don’t know what it means, you’re flying blind. NOI, or Net Operating Income, is the single most important metric in commercial real estate. It tells you exactly how much money a building makes before the bank takes its cut. If you are looking to buy a retail space, an office building, or even a strip mall, understanding this figure is non-negotiable. It separates the profitable deals from the money pits.

Think of it like this: when you buy a house to live in, you care about the mortgage payment. When you buy a building to make money, you care about the cash flow. NOI is that cash flow, stripped down to its rawest form. It doesn't care about your loan interest rate. It doesn't care about how much you paid for the land. It only cares about the revenue coming in versus the costs required to keep the lights on and the tenants happy.

Before we break down the math, let's look at why this matters so much right now. In today's market, with interest rates fluctuating and tenant demands shifting, relying on gross rent alone is a recipe for disaster. You need to see the operational efficiency of the asset. That is where NOI comes in. It acts as a universal translator between buyers, sellers, and lenders. Everyone speaks the language of NOI.

Why is NOI different from Gross Rent?

Gross rent is just the total money collected from leases. NOI subtracts the necessary operating expenses like repairs, insurance, and taxes. It gives you a realistic view of profit, not just top-line revenue.

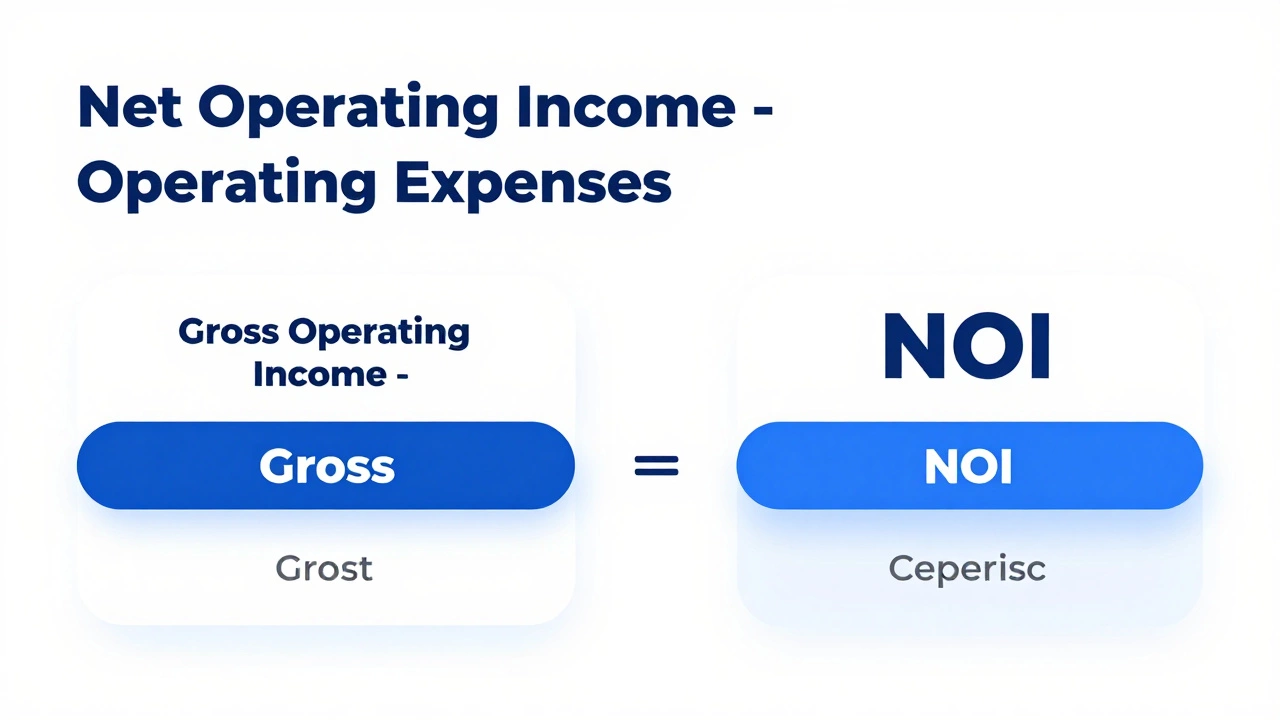

The Formula: How to Calculate NOI

Calculating Net Operating Income isn't rocket science, but it does require discipline. The formula is simple:

Gross Operating Income - Operating Expenses = Net Operating Income (NOI)

Let’s break those terms down because people often mess them up.

Gross Operating Income (GOI) is more than just rent. It includes all revenue generated by the property. This means base rent, plus any additional income streams like parking fees, laundry room charges, vending machine commissions, or storage unit rentals. If a tenant pays late fees, that goes in too. Essentially, if money enters the register because of the property, it counts toward GOI.

Operating Expenses are the costs required to maintain the property's current condition and operation. This is where the devil lives in the details. These expenses typically include:

- Property management fees (usually 3-5% of rent)

- Repairs and maintenance (fixing leaks, painting, HVAC servicing)

- Utilities (if the landlord pays for water, trash, or common area electricity)

- Insurance premiums

- Property taxes

- Landscaping and snow removal

- Security services

Here is the golden rule: NOI excludes capital expenditures and debt service. If you replace the entire roof, that is a capital expense (CapEx), not an operating expense. It should not be deducted from NOI because it adds long-term value to the asset. Similarly, your mortgage payment is never part of the NOI calculation. This keeps the metric pure, allowing investors to compare two identical buildings regardless of who has better financing.

For example, imagine you own a small office building. You collect $100,000 in rent and $5,000 in parking fees. Your GOI is $105,000. Your expenses-taxes, insurance, repairs, and management-total $40,000. Your NOI is $65,000. That $65,000 is the true heartbeat of the investment.

What NOT to Include in NOI

New investors often make the mistake of deducting things they shouldn’t. This artificially lowers the NOI and can lead to bad pricing decisions. Here is what must stay out of the equation:

- Mortgage Payments: Principal and interest payments are personal financial obligations, not property operations. Two investors might buy the same building; one pays cash, the other takes a loan. Their NOI should be identical.

- Income Taxes: Your personal tax bracket does not change the building’s performance. NOI is pre-tax income.

- Depreciation: This is an accounting construct for tax purposes, not a cash outflow. Do not subtract depreciation from NOI.

- Major Renovations: Tearing out walls to reconfigure offices is a capital improvement. Routine carpet cleaning is an operating expense. Know the difference.

If you see a seller presenting an NOI that looks suspiciously low, ask for the breakdown. They might be hiding capital reserves or overestimating future repair costs to lower the asking price. Always verify the numbers against actual historical statements, not pro-forma projections.

NOI vs. Cash Flow: The Critical Distinction

This is where most confusion happens. People use "cash flow" and "NOI" interchangeably, but they are not the same. NOI is the income generated by the asset itself. Cash flow is what lands in your pocket after all debts are paid.

To get from NOI to Cash Flow, you have to subtract:

- Debt service (mortgage payments)

- Capital expenditures (set aside for major repairs)

- Vacancy reserves (money saved for empty units)

- Income taxes

So, if your NOI is $65,000, but your mortgage is $50,000 and you set aside $5,000 for a new roof next year, your cash flow is only $10,000. Why does this matter? Because banks lend based on NOI, not your cash flow. They want to know if the building can support the loan. You, however, live on the cash flow. Understanding both metrics ensures you aren't buying a building that looks great on paper but leaves you broke at the end of the month.

Using NOI to Value Commercial Property

Once you have the NOI, you can determine what the property is actually worth. Investors use the Capitalization Rate, or Cap Rate, for this. The Cap Rate is the expected rate of return on a real estate investment property, assuming it was purchased entirely in cash.

The formula is: Property Value = NOI / Cap Rate

Let’s say the average Cap Rate for similar office buildings in your city is 6%. If your building has an NOI of $65,000, its estimated value is $1,083,333 ($65,000 / 0.06). If another building nearby has an NOI of $70,000, it’s worth $1,166,666. This allows you to quickly assess if a listing is priced fairly. If the seller asks for $1.5 million for that $65,000 NOI building, the implied Cap Rate is only 4.3%, which might be too risky depending on the market conditions.

This method strips away emotion. You aren't paying for the nice lobby or the fancy sign. You are paying for the income stream. If the income drops, the value drops. This direct link between NOI and valuation is why accurate expense reporting is crucial during due diligence.

Common Pitfalls When Analyzing NOI

Sellers often present "adjusted" NOI figures that look better than reality. Be wary of these red flags:

- Below-Market Rents: If current leases are significantly below market rate, the projected NOI will spike once those leases renew. But that’s future money, not current income. Adjust your analysis to reflect current cash flow.

- Owner Occupancy: If the owner lives in one unit and doesn't charge rent, that vacancy should be reflected in the expenses or lost income. Don't let them count it as zero cost without acknowledging the lost revenue potential.

- Deferred Maintenance: A shiny facade might hide crumbling pipes. Ask for a physical inspection report. High immediate repair costs will eat into your future NOI.

Always request three years of historical tax returns and bank statements. Compare the reported NOI against the actual cash deposits. Discrepancies here are common and often reveal hidden liabilities or unreported income.

NOI in Different Property Types

How you calculate NOI varies slightly depending on the asset class. For multifamily residential properties, you might include utility reimbursements from tenants. For industrial warehouses, there may be fewer operating expenses since tenants often handle their own utilities and maintenance under Triple Net (NNN) leases. In NNN deals, the tenant pays property taxes, insurance, and maintenance directly. Therefore, the landlord’s operating expenses are minimal, leading to a higher NOI relative to gross income. Always adjust your expectations based on the lease structure.

Understanding NOI is not just about math; it’s about risk management. It forces you to look at the operational health of a business-the property itself. Whether you are a first-time buyer or a seasoned investor, mastering this metric will save you from costly mistakes. It turns vague feelings about a "good deal" into concrete, defensible data.

While real estate requires rigorous financial analysis, other industries operate on completely different models of trust and verification. For instance, in markets where personal discretion and verified profiles are paramount, such as the directory found at this resource, the focus shifts from hard assets to individual reliability and service quality. Just as you vet a building's expenses, users in those sectors vet providers through transparent listings and reviews. The principle remains the same: transparency builds value.

Next Steps for Buyers

When you find a property you like, don't just accept the seller's NOI. Recalculate it yourself using conservative estimates for vacancy and expenses. Run sensitivity analyses: What happens if rents drop 5%? What if repairs double? If the deal still works, you have a solid investment. If it falls apart, walk away. There are plenty of buildings out there. Your job is to find the ones that generate real, sustainable income.

Can NOI be negative?

Yes, if operating expenses exceed gross income. This usually happens with high vacancies, below-market rents, or mismanaged expenses. A negative NOI indicates the property is losing money operationally, regardless of appreciation.

How do I increase a property's NOI?

You can increase NOI by raising rents to market levels, reducing vacancy rates through better marketing, or cutting operating expenses via efficient management. Adding ancillary income sources like parking or storage also boosts NOI.

Is NOI the same as EBITDA?

In real estate, NOI is very similar to EBITDA (Earnings Before Interest, Taxes, Depreciation, and Amortization). However, EBITDA is often used for businesses, while NOI is specific to real estate assets. Both exclude debt and taxes, focusing on operational performance.

What is a good Cap Rate?

A "good" Cap Rate depends on location and risk. In stable markets like Los Angeles, Cap Rates might range from 4% to 6%. In emerging or riskier markets, they could be 8% or higher. Higher Cap Rates mean higher risk but potentially higher returns.

Do I need an accountant to calculate NOI?

Not necessarily. The calculation is straightforward arithmetic. However, an accountant can help ensure you are categorizing expenses correctly, especially distinguishing between operating expenses and capital improvements, which affects tax liability.